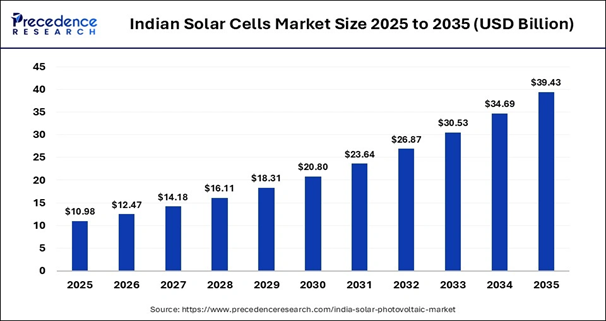

The Indian solar cells market size was calculated at USD 10.98 billion in 2025 and is predicted to increase from USD 12.47 billion in 2026 to approximately USD 39.43 billion by 2035, expanding at a CAGR of 13.67% from 2026 to 2035.

Indian Solar Cells Market Key Insights

- By material, the crystalline segment dominated the market in 2025.

- By material, the thin film segment is expected to be the fastest-growing segment during the forecast period.

- By product, the BSF segment led the market in 2025.

- By product, the HJT segment is expected to grow at the fastest CAGR in the coming years.

- By technology, the monocrystalline segment held the largest Indian solar cells market share in 2025.

- By technology, the CDTE segment is expected to witness the fastest growth over the studied years.

- By installation type, the utility segment contributed the biggest revenue share of the market in 2025.

- By installation type, the residential segment is expected to account for the highest growth in the forthcoming years.

- By end-user, the enterprise segment captured the major market share in 2024.

- By end-user, the industrial segment is projected to grow at the fastest CAGR in the market.

Role of AI Indian Solar Cells Market

Artificial Intelligence (AI) is becoming a transformative force in the development and commercialization of solar cells. Testing various materials, developing manufacturing techniques, and predicting long-term performance would particularly take months or years, but the emergence of AI tools has since accelerated the process. In the research domain, machine learning (ML) tools analyze huge amounts of datasets, pinpointing the best performance results.

In the manufacturing domain, integrating AI with computer vision systems enables real-time monitoring of processes and detects minor defects that can potentially compromise the whole batch.

Market Scope

| Report Coverage | Details |

| Market Size in 2025 | USD 10.98 Billion |

| Market Size in 2026 | USD 12.47 Billion |

| Market Size by 2035 | USD 39.43 Billion |

| Market Growth Rate from 2026 to 2035 | CAGR of 13.67% |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | Material, Product,Technology, and Installation Type |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Segmental Outlook of Indian Solar Cells Market

By Material Insights

Which Material Segment Dominated the Indian Solar Cells Market?

The crystalline segment dominated the market in 2025, due to higher efficiency levels, durability, and better performance in India’s diverse climate conditions, especially in high temperatures and dust exposure. Various government-backed projects also favor crystalline technology due to its mature supply chain and cost-effective nature. Monocrystalline cells are further favored for high-utility scale solar parks and large rooftop projects. The PLI has also prioritized its production, thus creating a strong domestic manufacturing base.

The thin film segment is expected to be the fastest-growing segment in the coming years, due to their lightweight structure, flexibility, and comparatively lower material costs, making them a popular choice for new-age applications such as building-integrated photovoltaics, portable power, and small-scale residential installation processes. Their advantage lies in their ability to perform better in diffuse light and high-temperature conditions.

By Product Insights

Why Did the BSF Segment Dominate the Indian Solar Cells Market?

The BSF segment contributed the biggest revenue share of the market in 2025, due to their low production costs, simplistic manufacturing processes, and a well-established supply chain. Several Indian companies continue to produce BSF cells in bulk, mainly because they are economical and suitable for large-scale and cost-sensitive utility projects. These types of cells are also popular in government-backed rural projects.

The HJT segment is expected to account for the highest growth in the forthcoming years, due to its ability to deliver higher efficiency, bifacial capability, and high performance in hot climates, making it attractive for premium as well as export-oriented projects. This segment continues to gain traction due to a growing interest in manufacturers and increasing research and development efforts.

By Technology Insights

How the Monocrystalline Segment Dominated the Indian Solar Cells Market?

How the Monocrystalline Segment Dominated the Indian Solar Cells Market?

The monocrystalline segment held a dominant revenue share of the market in 2025, as monocrystalline cells are produced using a single-crystal growing process, which lowers the entire unit cost and makes them more economical compared to other options. They offer high efficiency, durability, embedded energy, and lower operational costs, making them a popular option. Monocrystalline cells have a longer life span and provide space-saving benefits, further optimizing their efficiency.

The CDTE segment is expected to grow at the fastest CAGR in the coming years. This type of technology is better suited for India’s hot and humid temperatures, as these panels perform better than any other material. Additionally, it requires less material for production, which is a critical point as India aims to reduce its reliance on imported materials.

By Installation Type Insights

Which Installation Type Segment Led the Indian Solar Cells Market?

The utility segment led the market in 2025, due to the country’s aggressive push towards large-scale solar parks under national programs and schemes. Utility projects often benefit from economies of scale, lower costs per watt, and easier land acquisition in rural belts, thus making them attractive for both public and private investments. Various states, such as Rajasthan and Gujarat, have already become hubs for solar farms, boosting up utility scale installations.

The residential segment is expected to witness the fastest growth over the studied years. This growth is driven by decreased rooftop solar prices, supportive subsidies, net metering policies, and the rising cost of electricity in households. Increasing urbanization and the government’s push towards 40+ GW of rooftop capacity are further accelerating this segment’s growth. There are also EMI-based systems and leasing models that further increase awareness, making it accessible to middle-class households.

Recent Developments

- In July 2025, the Ministry of New and Renewable Energy (MNRE) asked power PSUs, such as NTPC, SJVN, NHPC, and Solar Energy Corporation of India (SECI), to modify their tenders to include the mandate of Indian made solar cells in their renewable energy bids. These PSUs are also acting as renewable energy implementing agencies (REIAs) in India’s goal to achieve 500 GW of non-fossil power capacity by 2030.

- In April 2025, India’s solar module manufacturing capacity has nearly doubled from 38GW to 74GW between March 2024 and March 2025. Furthermore, the country also commissioned its first 2GW of ingot and wafer manufacturing capacity. These figures are encouraging developments for India’s push towards greater domestic clean energy manufacturing.

Indian Solar Cells Market Companies

- Adani Solar is the solar manufacturing arm of the Adani Group, specializing in integrated solar PV manufacturing solutions. The company operates one of India’s largest solar cell and module manufacturing facilities with a strong focus on renewable energy innovation.

- Emmvee Solar is a leading Indian solar energy company known for manufacturing high-efficiency solar photovoltaic modules and solar water heating systems. The company serves residential, commercial, and industrial sectors with advanced clean energy solutions.

- Mahindra Susten Pvt. Ltd. is the clean-tech and renewable energy arm of Mahindra Group, offering solar EPC, project development, and renewable asset management services. The company focuses on delivering sustainable energy infrastructure across India and international markets.

- Sterling and Wilson Renewable Energy Ltd. is a global renewable EPC solutions provider specializing in solar power projects, hybrid energy systems, and energy storage solutions. The company has executed large-scale renewable energy projects across multiple continents.

- Tata Power Solar Systems Ltd. is one of India’s oldest and most trusted solar companies and a subsidiary of Tata Power. It provides solar rooftop solutions, utility-scale solar projects, and advanced solar manufacturing services.

- Vikram Solar Limited is a prominent Indian solar energy company engaged in manufacturing high-efficiency solar PV modules and offering EPC services. The company has a strong international presence and focuses on sustainable solar innovation.

- ReNew Power Pvt. Ltd. is one of India’s largest renewable energy companies, operating extensive wind and solar energy projects nationwide. The company is committed to accelerating India’s transition toward clean and sustainable energy generation.

- NTPC Ltd. is India’s largest integrated power utility company, actively expanding its renewable energy portfolio alongside conventional power generation. The company plays a major role in India’s energy security and green energy transition.

- Azure Power Global Ltd. is a leading independent solar power producer focused on developing and operating utility-scale solar projects in India. The company supports clean energy adoption through long-term sustainable power solutions.

{kind=link}