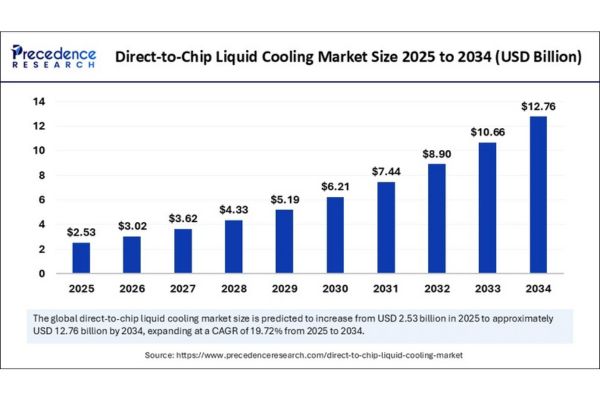

According to Precedence Research, the global direct to chip liquid cooling market size is expected to reach around USD 12.76 billion by 2034 from USD 2.11 billion in 2024, with a CAGR of 19.72%.

Direct-to-Chip Liquid Cooling Market Key Points

- North America dominated the global market with the largest market share of 40% in 2024.

- The U.S. direct-to-chip liquid cooling market is poised to grow at a solid CAGR of 21.8% from 2025 to 2030.

- Asia Pacific is projected to grow at the fastest CAGR of 22.7% during the forecast period.

- By cooling solution type, the single-phase liquid cooling segment contributed the highest market share of 66% in 2024.

- By cooling solution type, the two-phase liquid cooling segment is expected to witness the fastest growth during the predicted timeframe.

- By component cooling, the CPU cooling segment captured the biggest market share in 2024.

- By component cooling, the memory cooling segment will expand rapidly in the coming years.

- By liquid coolant type, the water-based coolants segment contributed the highest market share in 2024.

- By liquid coolant type, the dielectric fluids segment is expected to witness the fastest growth during the predicted timeframe.

- By application, the data center segment captured the biggest market share in 2024.

- By application, the high-performance computing (HPC) segment will expand rapidly in the coming years.

- By end-use, the telecommunications segment held a significant market share in 2024.

- By end-use, the oil and gas segment is projected to grow with the fastest CAGR during the forecast period.

How is AI Enhancing Efficiency in Direct-to-Chip Liquid Cooling Systems?

Artificial Intelligence (AI) plays a vital role in optimizing direct-to-chip liquid cooling by enabling real-time monitoring and predictive maintenance. AI algorithms analyze temperature, pressure, and flow rate data from sensors embedded in the cooling systems to dynamically adjust coolant distribution, ensuring optimal thermal performance.

This smart regulation not only reduces energy consumption but also enhances cooling precision for high-performance computing environments such as data centers and AI training clusters.

AI-driven analytics help forecast potential failures and performance degradation in cooling systems before they occur. By continuously learning from historical and real-time data, AI can predict component wear, recommend maintenance schedules, and detect anomalies early.

This proactive approach minimizes downtime, extends system life, and supports the scalability of advanced computing infrastructure, making AI a key enabler in the evolution of direct-to-chip liquid cooling technology.

What is Direct-to-Chip Liquid Cooling?

Direct-to-chip (D2C) liquid cooling is an advanced thermal management technology where liquid coolant is directly delivered to the surface of high-heat-generating components such as CPUs, GPUs, and memory chips. Unlike traditional air cooling, this method uses cold plates mounted on the chips, through which coolant flows to absorb and carry away heat. The cooled liquid is then recirculated, often using a closed-loop system, to maintain optimal operating temperatures.

Why is it Gaining Popularity?

D2C liquid cooling is becoming increasingly essential in high-density computing environments like data centers, hyperscale facilities, and AI/ML workloads. It offers significant advantages such as higher cooling efficiency, reduced energy consumption, lower noise levels, and the ability to handle higher thermal design power (TDP) loads. As computing power demands rise and sustainability becomes a priority, D2C cooling provides a scalable and environmentally friendly alternative to traditional cooling systems.

Market Scope

| Report Coverage | Details |

| Market Size by 2034 | USD 12.76 Billion |

| Market Size in 2025 | USD 2.53 Billion |

| Market Size in 2024 | USD 2.11 Billion |

| Market Growth Rate from 2025 to 2034 | CAGR of 19.72% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2024 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | Cooling Solution Type, Component Cooling, Liquid Coolant Type, Application, End Use, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Regional Outlook of Direct to Chip Liquid Cooling Market

North America

North America dominates the direct-to-chip liquid cooling market, holding about 40% market share in 2024. The region’s leadership is driven by robust growth in data centers, high adoption of high-performance computing, and significant investments in technological innovation.

The United States is the key player, fueled by government support for exascale computing, the rapid rise of AI workloads, and a strong push for energy-efficient solutions. Despite facing challenges from tariffs affecting hardware and supply chains, the region’s demand for sustainable and high-performance cooling solutions remains strong.

Asia Pacific

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of 22.7% through 2034. Rapid digital transformation, widespread adoption of advanced technologies, and a strong focus on sustainability are driving market growth. Countries like China, Japan, India, and Singapore are investing heavily in data center infrastructure and innovation.

China leads with its booming cloud applications sector, while Japan excels with high-value data centers. Government initiatives promoting green and energy-efficient technologies further accelerate adoption across the region.

Europe

Europe is experiencing transformative growth in the direct-to-chip liquid cooling market, primarily due to increasing demand for energy-efficient and high-density computing solutions. The region benefits from stringent regulatory support for green technologies and significant investments in R&D.

Germany stands out as a major market, thanks to its emphasis on sustainability and the expansion of data center infrastructure. European enterprises are rapidly adopting these solutions to manage high heat loads and enhance renewable energy usage in data centers.

Segmental Analysis of the Direct-to-Chip Liquid Cooling Market

Cooling Solution Type Insights

The market is primarily segmented into single-phase and two-phase liquid cooling solutions. In 2024, the single-phase segment dominated with over 66% market share, favored for its efficient heat dissipation, cost-effectiveness, and operational simplicity—making it ideal for data centers and high-performance computing.

However, the two-phase segment is expected to grow fastest due to its superior ability to manage high heat loads, making it suitable for advanced computing environments requiring optimal thermal management.

Component Cooling Insights

CPU cooling leads the market as CPUs generate significant heat, especially with the rise of AI, IoT, and high-performance computing workloads. The need for effective thermal management to maintain CPU stability and performance is driving adoption.

The memory cooling segment is also growing, propelled by the increasing use of high-speed, high-capacity memory chips in servers and AI applications, which demand efficient cooling to prevent overheating and ensure reliability.

Liquid Coolant Type Insights

Water-based coolants held the largest share in 2024, thanks to their high thermal conductivity, cost-effectiveness, and sustainability benefits. These coolants are widely used in data centers and enterprise IT due to their efficiency in reducing energy consumption.

Dielectric fluids are the second-largest segment, valued for their safety (preventing electrical shorts) and suitability for high-density electronics, offering efficient heat transfer and energy-saving benefits.

Application Insights

The data center segment captured the largest market share in 2024, as traditional air-cooling methods struggle to manage the heat generated by modern, high-density workloads. The high-performance computing (HPC) segment is expected to lead future growth, driven by the expanding use of AI, machine learning, and research applications that generate intense heat and require advanced cooling solutions to maintain performance and prevent thermal throttling.

End Use Insights

Telecommunications was the largest end-use segment in 2024, with the rapid rollout of 5G networks and the proliferation of edge data centers increasing demand for efficient cooling.

The oil and gas sector are also a key adopter, using direct-to-chip liquid cooling to support digital oilfield technologies and manage the high temperatures of downhole and subsea applications.

Direct-to-Chip Liquid Cooling Market Companies

ZutaCore: Pioneers waterless, two-phase direct-to-chip cooling, enabling high-density, energy-efficient data centers, especially for AI and HPC applications.

Advanced Micro Devices (AMD): Produces high-performance processors that drive demand for advanced cooling; collaborates with cooling providers to ensure compatibility and efficiency.

Schneider Electric: Offers integrated liquid cooling solutions and infrastructure for data centers, focusing on energy efficiency and sustainability.

JetCool Technologies: Specializes in microconvective direct-to-chip cooling using targeted jets, supporting high-power AI and HPC systems with reduced energy and water use.

LiquidStack: Develops advanced two-phase liquid cooling solutions for hyperscale and enterprise data centers, addressing high thermal loads.

Iceotope Technologies: Provides chassis-level and direct-to-chip liquid cooling, delivering efficient, low-maintenance solutions for compute-intensive environments.

CoolIT Systems: A leading supplier of scalable direct-to-chip cooling systems for data centers and HPC, known for innovation and broad industry adoption.

Asetek: Offers patented direct-to-chip liquid cooling technology for data centers and HPC, enabling efficient thermal management and energy savings.

Fujitsu: Incorporates direct-to-chip cooling into its servers and data center solutions, focusing on energy efficiency and sustainability.

Chilldyne: Develops negative pressure direct-to-chip cooling systems to minimize leak risks and provide reliable cooling for data centers and HPC.

Vertiv Holdings Co: Supplies modular, efficient direct-to-chip cooling products for high-capacity data centers, supporting advanced computing needs in major markets.

Source: https://www.precedenceresearch.com/direct-to-chip-liquid-cooling-market

{kind=link}