Constant innovations and development in packaging processes and materials s enhance yield and minimize costs, making advanced packaging solutions more attractive. The key players operating in the market are focused on adopting inorganic growth strategies like acquisition and merger to develop advance technology for manufacturing semiconductor & IC packaging materials which is estimated to drive the global semiconductor & IC packaging materials market over the forecast period.

Semiconductor & IC Packaging Materials Market: Enhance Device Performance

Semiconductor packaging refers to the process of enclosing semiconductor devices (like integrated circuits, or ICs) to protect them and connect them to other electronic components. This packaging is crucial for ensuring the functionality, reliability, and performance of electronic devices. Semiconductor & IC packaging protects delicate semiconductor materials s from environmental factors such as moisture, dust, and physical damage. It provides the necessary connections to other circuit elements.

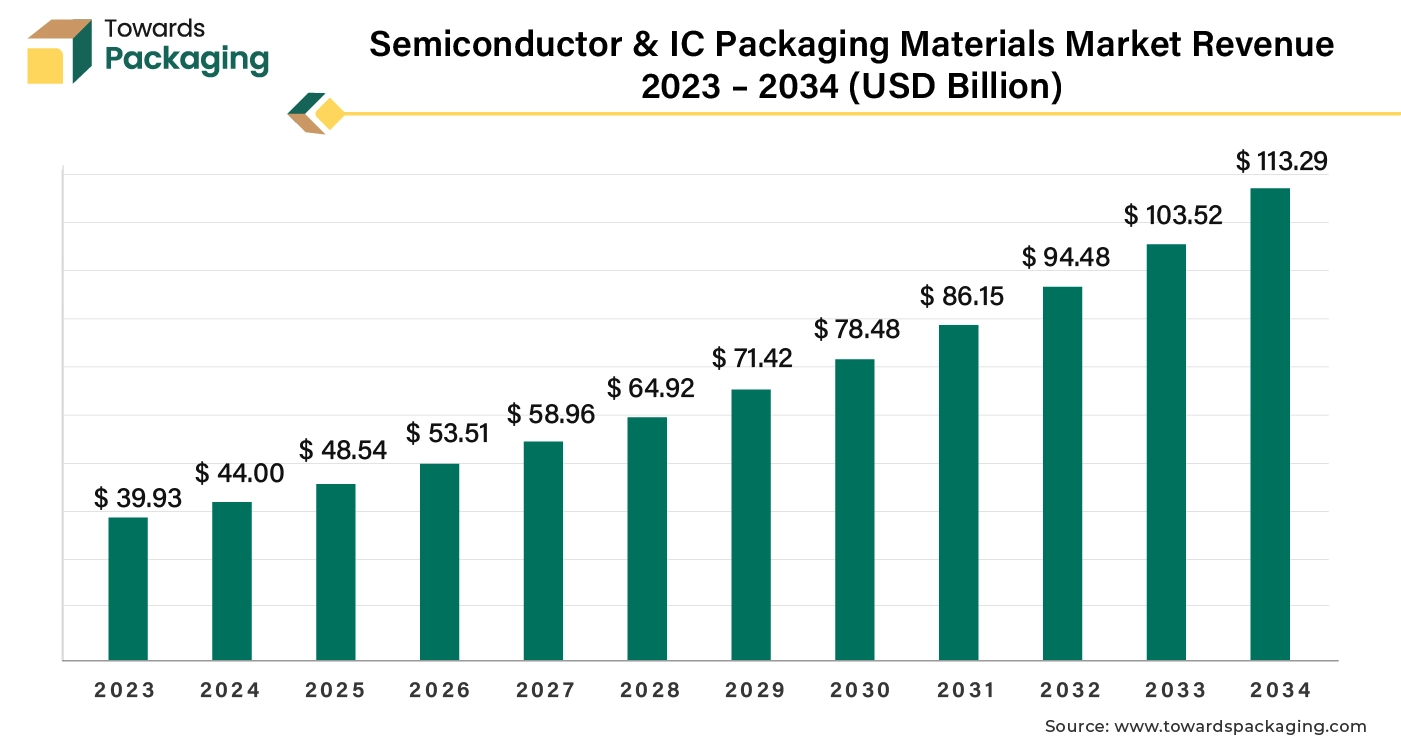

The global semiconductor & IC packaging materials market size reached US$ 39.93 billion in 2023 and is projected to hit around US$ 113.29 billion by 2034, expanding at a CAGR of 10.2% during the forecast period from 2024 to 2033.

The packaging facilitates the integration of ICs into electronic systems through pins or pads. Semiconductor and ICs generate heat during operation, and packaging plays a vital role in dissipating this heat to maintain performance and prevent failure. Semiconductor & IC packaging adds structural integrity, helping to withstand mechanical stresses during manufacturing and use.

5 Key Factors Driving Semiconductor & IC Packaging Materials Market Growth

- The key players operating in the market are focused on geographic expansion and launching their brand in other countries which is expected to drive the growth of the semiconductor & IC packaging materials market in the near future.

- Increasing focus on cost reduction and production efficiency can drive the specialty market growth further.

- Emerging markets and trends for semiconductor & IC packaging materials is expected to drive the growth of the global semiconductor & IC packaging materials market over the forecast period.

- Increasing regulatory support is estimated to drive the growth of the market over the forecast period.

- Increasing in adoption of the advanced technology for the production of semiconductor & IC packaging materials is estimated to drive the growth of the global semiconductor & IC packaging materials market in the near future.

Rising Demand and Innovation for Electronics

With the increasing use of tablets, smartphones, and consumer electronics, there is a heightened demand for advanced and next-generation semiconductor packaging. The proliferation of IoT devices is driving the need for smaller, more efficient packaging solutions. The key players operating in the market are focused on innovating and launching new electronic devices which require compact semiconductor and IC packaging materials, which has created lucrative opportunity for the growth of the semiconductor & IC packaging materials market in the near future.

Organic Substrate to Lead Market in 2023

The organic substrate segment held a dominant presence in the semiconductor & IC packaging materials market in 2023. Organic substrates offer excellent thermal stability, electrical performance, and reliability, making them suitable for advanced applications. They are generally more affordable compared to traditional materials like ceramics, facilitating wider adoption in various applications. Organic substrates are lighter than traditional materials, contributing to the overall reduction in weight for electronic devices, which is essential for portable technologies. The organic semiconductors have ability to manage heat effectively.

Small Outline Package (SOP) to Hold Significant Share

The small outline package (SOP) segment accounted for a significant share of the semiconductor & IC packaging materials market in 2023. Small Outline Package (SOPs) are designed to occupy less board space, making them ideal for compact electronic devices, which is crucial in consumer electronics and mobile applications.

Small Outline Packaging (SOPs) are easier to handle during assembly processes, contributing to faster production times and reduced labor costs. They generally have lower manufacturing costs compared to other packaging types, making them attractive for mass production.

Consumer Electronics to Hold a Notable Share in the Market

The consumer electronics segment registered its dominance over the global semiconductor & IC packaging materials market in 2023. The demand for smaller, more compact devices drives the need for advanced packaging solutions that save space without compromising performance. IC packaging materials can be adapted for a wide range of applications, from smartphones to home appliances, making them suitable for diverse consumer electronics. High-performance packaging materials ensure efficient heat dissipation and electrical connectivity, crucial for the functioning of modern electronics.

Asia’s Tech Innovation to Support 90% of Dominance

Asia Pacific region held the dominating share of the semiconductor & IC packaging materials market in 2023. Countries like China, Japan, and South Korea have advanced manufacturing infrastructures, allowing for mass production of electronics at competitive prices. A rapidly growing middle class and increasing disposable income in countries like India and Southeast Asia boost demand for consumer electronics. Major tech companies in the region invest heavily in research and development, driving innovation in consumer electronics. The presence of a well-developed supply chain and logistics network facilitates quick turnaround times and cost efficiency.

Research & Development in North America to Promote Growth

North America region is anticipated to grow at the fastest rate in the semiconductor & IC packaging materials market during the forecast period. The United States has the biggest market share in the North American semiconductor industry and has seen the fastest growth throughout the projected period due to its significant R&D investments, cutting-edge technological infrastructure, and robust ecosystem of semiconductor businesses. Big American semiconductor businesses like Texas Instruments, Qualcomm, and Intel are the ones driving continuous innovation in packaging technology.

About The Author

Asmita Singh is a renowned author and consultant in the packaging industry, known for her deep passion for knowledge discovery and commitment to delivering actionable insights. With extensive experience in implementing advanced research methodologies, Asmita generates high-quality data and meaningful results that drive innovation and efficiency in packaging solutions. Her expertise spans the globe, offering valuable consulting services to businesses aiming to enhance their packaging strategies. Asmitas work is characterized by a dedication to excellence and a keen understanding of the latest trends and technologies shaping the future of packaging.

to protect them){kind=link}