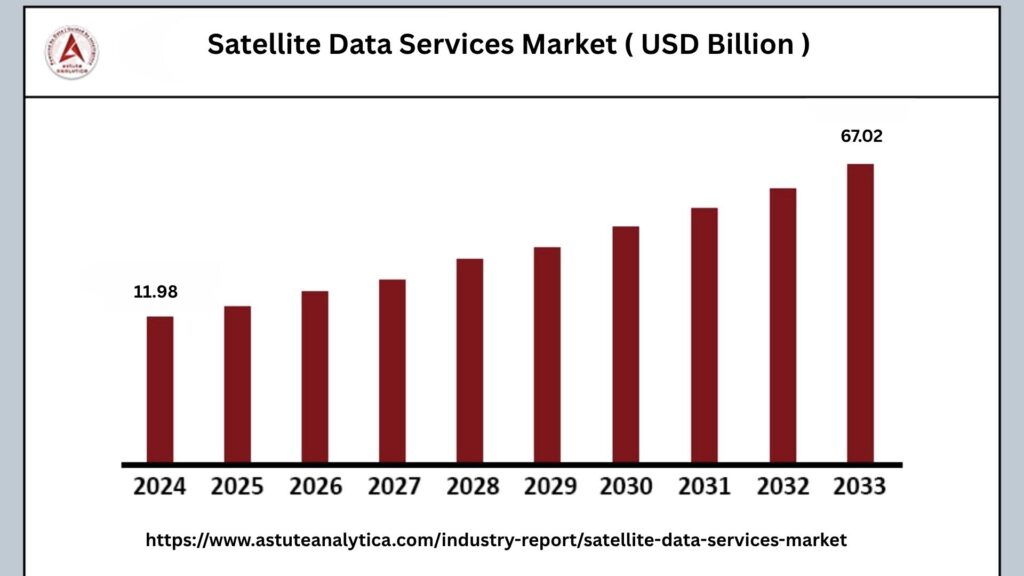

The global satellite data services market was valued at US$ 11.98 billion in 2024 and is projected to reach US$ 67.02 billion by 2033, reflecting a Compound Annual Growth Rate (CAGR) of 22.69% during the forecast period from 2025 to 2033.

Satellite data services encompass the comprehensive process of collecting, processing, and distributing information captured by satellites orbiting the Earth. These satellites gather a wide array of data that offers valuable insights into numerous aspects of our planet. This includes monitoring weather patterns, tracking changes in land use, assessing environmental conditions, and observing human activities.

The global satellite data services market is currently experiencing rapid growth, a trend that is expected to persist in the foreseeable future. Several interrelated factors are driving this expansion. Chief among them is the rising demand for Earth observation data across a variety of sectors, including agriculture, defense, environmental management, and telecommunications. As industries increasingly rely on precise and timely satellite data to enhance operational efficiency and sustainability, the market continues to broaden its reach.

Satellite Data Services Market Key Takeaways

- In 2024, the data analytics segment emerged as the dominant service within the global satellite data services market, capturing the largest share of 57.95%.

- From an industry perspective, the defense and security sector led the satellite data services market, accounting for the highest share of 28.07%.

- Regarding technology, optical and radar imaging technologies held the largest share of 35.47% in the global satellite data services market in 2024.

- In terms of application, the terrestrial satellite data range segment dominated the market with a commanding share of 74.94%.

Regional Analysis

North America Dominated the Satellite Data Services Market

The North American satellite data services market is widely regarded as a global benchmark due to its highly advanced infrastructure and strong government involvement. The United States, in particular, plays a dominant role with significant federal contracts fueling market growth.

- Leading Commercial Players and Strategic Contracts: North America’s leadership in the satellite data services sector is further strengthened by prominent commercial companies like Planet Labs and Maxar Technologies. These firms have secured substantial government contracts, leveraging their extensive satellite fleets to provide high-resolution imagery and real-time data services.

- Seamless Integration and Diverse Applications: The region benefits from a sophisticated digital infrastructure that facilitates the seamless integration of satellite-derived insights into various operational workflows. This integration supports critical applications such as precision agriculture, enabling farmers to optimize crop yields through detailed land and weather data. In disaster response efforts, satellite data provides timely and accurate information that aids emergency planning and resource allocation.

- Enhanced Service Reliability through Low Earth Orbit Constellations: A key factor enhancing the reliability and effectiveness of North America’s satellite data services is the widespread deployment of low Earth orbit (LEO) satellite constellations. These constellations offer significant advantages, including low latency and high data transmission rates, which are essential for time-sensitive applications such as real-time surveillance and rapid disaster response.

Europe to Lead the Satellite Data Services Market

Europe’s satellite data services market is characterized by robust governmental backing and strategic investments that have laid a solid foundation for its development.

- Copernicus’s role in Earth Observation: A central element defining Europe’s satellite data landscape is the Copernicus program, the EU’s flagship Earth observation initiative. Copernicus provides open and free access to a vast array of high-quality satellite data covering land, ocean, and atmospheric monitoring. This comprehensive framework supports both public sector applications and commercial innovations by offering reliable, standardized data that users across sectors can readily utilize.

- Focus on Sustainability and Climate Monitoring: Sustainability and climate monitoring are at the heart of Europe’s satellite data services market growth. The region is actively using satellite data to track environmental changes, assess the impact of climate policies, and support the transition to a low-carbon economy.

- Integration of Satellite Data into Policy-Making and Urban Planning: European governments prioritize embedding satellite data insights into policy-making processes to promote sustainable development. By integrating geospatial information into regulatory frameworks and urban planning strategies, authorities can optimize land use, manage natural resources efficiently, and enhance disaster preparedness.

Rapid Growth of the Asia-Pacific Satellite Data Services Market

The Asia-Pacific region is currently witnessing the fastest expansion in the satellite data services market, driven by a combination of aggressive government initiatives, increasing commercial adoption, and a growing demand for data-centric solutions across various sectors.

- Strong Government Support and Infrastructure Investment: Governments in key Asia-Pacific countries like China, India, and Japan are playing a pivotal role in accelerating market growth by investing heavily in satellite infrastructure and advanced data analytics platforms. These initiatives include the deployment of dedicated satellites designed for specific applications such as agricultural monitoring, flood risk assessment, and urban development planning.

- Expanding Commercial Adoption in Agriculture and Beyond: The agriculture segment within the Asia-Pacific satellite data market is particularly dynamic, with a projected compound annual growth rate (CAGR) of 21.7%. This rapid growth is fueled by farmers and agribusinesses increasingly adopting satellite-based solutions to enhance productivity, monitor crop health, and manage resources more sustainably.

- Regional Collaboration and Future Outlook: The Asia-Pacific satellite data services market benefits from strong regional collaboration, where countries share knowledge, infrastructure, and best practices to maximize the impact of satellite data applications. Looking ahead, continued investments in satellite constellations, enhanced data analytics capabilities, and supportive policy frameworks are expected to sustain the region’s rapid growth trajectory.

Top Trends Escalating the Satellite Data Services Market

Integration of Artificial Intelligence for Advanced Satellite Data Analytics Solutions: The integration of artificial intelligence (AI) into satellite data analytics is revolutionizing how satellite imagery and data are processed and interpreted. AI algorithms enable the automation of complex data analysis tasks, such as identifying patterns, detecting anomalies, and extracting meaningful insights from vast datasets. This advanced processing capability allows for faster and more accurate decision-making across various sectors, including agriculture, defense, environmental monitoring, and urban planning.

Expansion of Cloud-Based Platforms: Cloud-based platforms are increasingly becoming the backbone of satellite data management, offering scalable solutions for the storage, processing, and distribution of massive volumes of satellite imagery. These platforms provide flexible infrastructure that can handle fluctuating data loads and enable seamless collaboration among global users. The accessibility of cloud resources accelerates data analysis workflows by allowing users to process large datasets without the limitations of local hardware.

Deployment of Advanced Onboard Sensors: The deployment of advanced onboard sensors on satellites is significantly enhancing data collection capabilities. These sensors are designed to capture high-resolution images and multispectral, hyperspectral, and synthetic aperture radar (SAR) data, providing detailed and diverse information about the Earth’s surface and atmosphere.

Growing Demand for High-Resolution Satellite Imagery: There is an escalating demand for high-resolution satellite imagery in sectors where critical decisions depend on precise and timely geospatial information. Industries such as defense, agriculture, urban development, disaster management, and energy increasingly rely on detailed imagery to monitor assets, assess risks, and optimize operations.

Increasing Government and Military Reliance: Government and military agencies are placing greater emphasis on real-time geospatial intelligence derived from satellite data to enhance national security and operational readiness. Continuous satellite monitoring provides critical situational awareness, enabling timely detection of threats, border surveillance, and support for tactical missions. The ability to access and analyze real-time satellite data supports informed decision-making in complex and dynamic environments.

Rapid Technological Advancements: Technological progress in satellite design, miniaturization, and launch capabilities has led to more cost-effective and frequent satellite data acquisition. The development of smaller, lighter satellites and reusable launch vehicles has reduced the cost barriers traditionally associated with satellite deployment. These advancements facilitate the launch of large constellations that provide near-continuous coverage and more frequent data updates.

Satellite Data Services Market Segmentation

By Service

In 2024, the data analytics segment emerged as the dominant force in the global satellite data services market, commanding the largest share at 57.95%. This substantial lead reflects the growing importance of transforming raw satellite data into actionable insights that can support a wide range of industries and applications. As organizations and governments increasingly rely on timely and precise information, the demand for advanced data analytics solutions continues to intensify, driving the segment’s significant market presence.

Looking ahead to the forecast period from 2025 to 2033, the data analytics segment is expected to achieve the highest compound annual growth rate (CAGR) of 23%. This remarkable growth trajectory is fueled by ongoing technological advancements and the urgent need for real-time data processing. One key development contributing to this trend is the proliferation of edge computing capabilities, which have dramatically reduced the latency between satellite data acquisition and insight generation to under 15 minutes.

By Industry

The defense and security sector holds a commanding position in the satellite data services market, accounting for the largest share of 28.07%. This leading role underscores the vital dependence of national security operations on space-based assets. Military organizations around the world extensively utilize dedicated reconnaissance satellites that provide continuous monitoring of strategic locations, often capturing updated imagery every 90 minutes. This frequent surveillance capability is essential for maintaining situational awareness, detecting potential threats, and supporting tactical decision-making.

Furthermore, the integration of advanced technologies such as artificial intelligence (AI) and machine learning (ML) has transformed the way satellite data is analyzed within the defense sector. These intelligent systems enable defense agencies to process vast amounts of satellite imagery and extract actionable insights more efficiently and accurately than ever before. By automating pattern recognition and anomaly detection, AI and ML significantly enhance the effectiveness of intelligence gathering and threat assessment.

By Application

The terrestrial satellite data range segment holds the largest share in the global satellite data services market, accounting for 74.94% of the total market. This dominant position highlights the critical importance of terrestrial data in various applications. The segment is also expected to experience a robust compound annual growth rate (CAGR) of 22.93% throughout the forecast period, indicating rapidly increasing demand.

This growth is driven by the rising need for detailed and granular land intelligence, which is becoming essential across industries such as agriculture, environmental monitoring, and mining. Notably, 2025 is set to be a milestone year with the launch of hyperspectral satellites. These advanced satellites will possess the capability to identify distinct mineral signatures, significantly enhancing mining exploration efforts and further fueling the segment’s expansion.

Recent Developments in the Satellite Data Services Market

Arabsat and First Gulf Company Partnership for VSAT Services in Saudi Arabia: In July 2025, Arabsat announced a strategic collaboration with First Gulf Company (FGC) to enhance satellite communication services within Saudi Arabia. This partnership combines Arabsat’s advanced Geostationary Orbit (GEO) Ku-band infrastructure with FGC’s strong operational expertise. Together, they aim to deliver high-capacity, fully managed VSAT and IP-based data services.

T-Mobile Expands Satellite-to-Cell Network with Full Data Services: In June 2025, T-Mobile confirmed that its innovative satellite-to-cell network, branded as T-Satellite, will expand its capabilities to include full data services starting October 1, 2025. This development marks a significant milestone following the initial rollout of messaging services scheduled for July 2025.

Safaricom and Starlink Launch Satellite Internet Services in Kenya: In December 2024 will witness Safaricom’s entry into the satellite Internet market, coinciding with a similar launch by Elon Musk’s Starlink in Kenya. These satellite Internet offerings represent a potential game-changer for the country’s telecom landscape, which has long struggled with coverage gaps, particularly in rural regions.

Major Players in the Satellite Data Services Market

- Airbus SE

- ORBCOMM

- Boeing

- GomSpace

- Lockheed Martin Corporation

- Maxar Technologies

- Orbital Insight

- Planet Labs

- SURREY SATELLITE TECHNOLOGY LTD

- Thales

- York Space Systems

- Other Prominent Players

Market Segmentation Overview:

By Service

- Data Analytics

- Land and Water State of Agriculture and Environment Analysis

- Historic Agricultural and Environmental Metrics

- Identify Trends from Satellite Indices

- Crop Performance

- Natural Resource Management

- Risk Management

- Image Data

- Geospatial

- Others

By Technology

- Optical and Radar Imagery Technology

- Synthetic Aperture Radar (SAR) Active Remote Sensing Technology

- Geospatial Technology

- Others

By Application

- Terrestrial Satellite Data Range

- Agriculture Harvest Monitoring & Field Segmentation

- Security Surveillance

- Infrastructure & Construction Monitoring

- Mapping of Areas Affected by Natural Disasters

- Interferometry

- Oil Pipeline Monitoring

- Maritime Satellite Data Range

- Prevention of Illegal Fishing

- Coastal Security

- Monitoring Port and Sea Traffic

- Ice Monitoring and Iceberg Tracking

- Natural and Man-Made Catastrophe Responses

- Others

By Industry

- Energy & Power

- Mining And Mineral Exploration

- Oil And Gas Operation

- Agriculture

- Environmental

- Engineering & Infrastructure

- Ocean

- Forestry

- Transportation & Logistics

- Insurance and Finance

- Media And Entertainment

- Others

By Geography

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

{kind=link}