The global renewable energy asset management market size was USD 9.85 billion in 2024, estimated at USD 11.18 billion in 2025 and is anticipated to reach around USD 35.07 billion by 2034, expanding at a CAGR of 13.54% from 2025 to 2034. Growth is propelled by the rapid buildout of renewables capacity, the mainstreaming of SaaS-based portfolio platforms, and intensifying sustainability mandates that demand measurable performance, compliance, and returns.

Quick insights

- Market size & trajectory: USD 9.85 billion (2024) to USD 35.07 billion (2034); 13.54% CAGR (2025–2034).

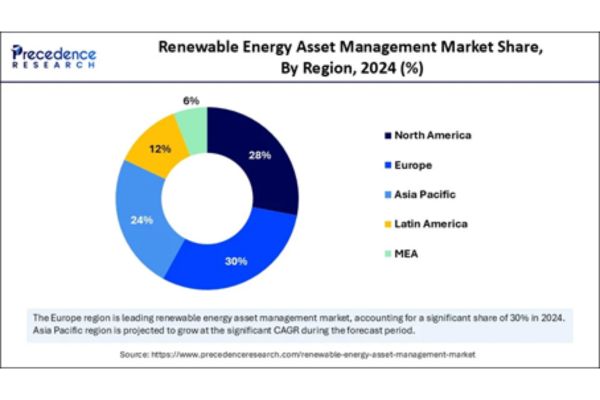

- Regional leader (2024): Europe at ~30% share (USD 2.96 billion), supported by robust policy frameworks and digital infrastructure; Asia Pacific is set to be the fastest-growing region through 2034.

- Energy source: Solar power led in 2024 and is expected to sustain leadership amid utility-scale and distributed buildouts.

- Functionality/activity: Performance analytics held the largest 2024 share (~25%), while predictive & preventive maintenance is poised for the fastest growth.

- Deployment model: Cloud-based/SaaS captured the largest share in 2024 (~45%); hybrid architectures to post notable growth through 2034.

- End-user dynamics: Independent power producers (IPPs) led in 2024; industrial & commercial energy buyers to grow notably as on-site and off-site procurement scales.

Market overview: scale, software, and smarter O&M

A decade of aggressive capacity additions has ushered in an era where operational excellence is won in software. Asset owners and operators are centralizing SCADA/IoT telemetry, combining it with AI/ML-driven analytics to unlock actionable insights across performance baselines, degradation patterns, and weather-driven variability. Platforms blend real-time condition monitoring with predictive maintenance, elevating uptime and extending asset life, particularly critical as portfolios become multi-technology and multi-geography.

Macro tailwinds amplify this shift: the IEA projects renewable electricity generation to exceed 17,000 TWh by 2030, up roughly 90% from 2023, underscoring the need for scalable, automated asset oversight. As sustainability-linked financing and disclosure frameworks tighten, asset management systems are now pivotal for compliance, auditability, and investor-grade reporting.

How is AI reshaping the renewable energy asset management market?

AI is becoming the operations copilot. From fault pattern recognition in wind gearboxes to soiling and clipping models on PV strings, operators are deploying AI to triage alerts, reduce false positives, and prioritize work orders. Grid-aware analytics support curtailment strategies, while forecasting models improve bid/dispatch decisions and PPA settlement accuracy. The net effect: higher yield, lower O&M cost, and faster decision cycles, with measurable gains compounding across large fleets.

Regional outlook: why Europe leads, and where the next wave comes from

Europe commanded about 30% of global revenue in 2024 (USD 2.96 billion), buoyed by a broad renewables base, strong policy coherence, and digital maturity. With more than 47% of EU electricity production sourced from renewables in 2024, operators face complex integration and lifecycle management needs spanning performance monitoring, grid coordination, and compliance, fertile ground for advanced analytics and SaaS-led oversight.

Asia Pacific is the growth engine. Massive annual installations, led by China, India, Japan, and Australia, are expanding asset counts and diversifying portfolios. This creates urgency for automated benchmarking, predictive maintenance, and cloud-native portfolio control, particularly as corporate buyers scale 24/7 clean procurement strategies. The region’s combination of high-capacity additions, distributed energy proliferation, and government-led digitalization will make it the fastest-growing market through 2034.

Segment analysis: where value consolidates

Energy source

Solar retained leadership in 2024 and is expected to sustain it, driven by utility-scale pipelines and rooftop proliferation. Mature supply chains, improving component reliability, and repeatable BOS patterns make solar uniquely amenable to data-driven O&M, with strong ROI on soiling analytics, inverter health, and string-level diagnostics.

Functionality / activity

- Performance analytics & reporting led in 2024 (25% share) as owners standardize KPI frameworks to quantify losses, highlight repowering triggers, and benchmark across fleets.

- Predictive & preventive maintenance is set to expand the fastest as condition-based strategies replace calendar-based routines, cutting unplanned downtime and extending component life.

Deployment model

- Cloud-based/SaaS accounted for 45% in 2024 as enterprises favor rapid deployment, centralized data lakes, and elastic compute for fleet-scale analytics.

- Hybrid architectures will grow notably, balancing edge latency for controls with cloud scale for analytics, especially in distributed assets and markets with data-sovereignty requirements.

End-user

- IPPs led in 2024, reflecting their large, diversified fleets and need for centralized dashboards, market integration, and contract compliance.

- Industrial & commercial energy buyers are poised for notable growth amid on-site generation, off-site PPAs, and energy-as-a-service, increasing demand for buyer-facing performance guarantees and meter-to-PPA settlement tools.

Recent developments: signals of a maturing, software-first ecosystem

- Exus Renewables secured a new 307 MW asset management mandate from Ingka Investments (IKEA’s investment arm), expanding third-party oversight across 23 wind farms and a grid project in seven European countries, evidence of deepening specialization in outsourced asset management.

- IBM launched Maximo Renewables (general availability), packaging real-time monitoring, predictive maintenance, and performance analytics in a purpose-built solution for renewable fleets, strengthening the enterprise-grade software stack for operators.

- Macquarie Asset Management introduced Aula Energy to develop and operate utility-scale solar, wind, and hybrid battery projects in Australia and New Zealand, aligning capital, development, and long-term operations within managed digital frameworks.

- ALTÉRRA announced a USD 100 million co-investment in Evren (India), catalyzing capacity scale-up across one of the world’s fastest-growing renewable markets, spotlighting investor confidence in digital-ready portfolios.

Case in focus: scaling third-party asset management across borders

Challenge: A pan-European renewable investor needed a unified approach to monitoring, reporting, and optimizing a multi-country wind portfolio with diverse regulatory regimes and operating conditions.

Approach: Partnering with a specialist asset manager expanded standardized performance analytics, lifecycle planning, and O&M oversight across 23 wind farms plus a grid asset.

Outcome: Centralized dashboards created comparable KPIs, accelerated repowering and maintenance decisions, and strengthened grid integration performance, the core blueprint for cross-border expansion without sacrificing operational depth.

Challenges and cost pressures: what could slow adoption?

Despite strong momentum, high upfront implementation costs, from IoT sensorization and digital twin model development to integration across heterogeneous data protocols, can constrain deployment, particularly for smaller developers. Fragmented data standards, legacy SCADA compatibility issues, and the need to harmonize multi-vendor fleets can elongate rollouts and add integration risk. Vendors that deliver open architectures, interoperability, and time-to-value will be best positioned to neutralize these headwinds.

Opportunity & trend watch: where will the next wave of value be created?

- Hybrid portfolios, unified control: Integrated solar-wind-storage assets will intensify demand for platforms that coordinate dispatch, capture arbitrage, and minimize curtailment across markets.

- Predictive everything: Edge-to-cloud telemetry fused with ML-driven failure prediction will trim truck rolls, extend component life, and optimize spare parts logistics.

- ESG-grade reporting: Investor and regulatory scrutiny elevates the need for audit-ready, granular performance and emissions data, embedding asset management software into the finance, risk, and sustainability stack.

- Grid flexibility & VPPs: Growth in microgrids and virtual power plants will favor systems that orchestrate distributed assets and align them with market signals in near-real time.

Renewable Energy Asset Management Market Top Companies

- ABB

- ABB-YY Grid

- Bosch Rexroth (Bosch)

- C3.ai

- Delta Electronics

- Eaton

- Emerson Electric

- Fuji Electric

- GE Renewable Energy

- Hitachi Energy

- Honeywell (Honeywell Process Solutions)

- Huawei Digital Power (HUAWEI)

- Ingeteam

- Mitsubishi Electric

- NARI Group (NARI-Grid)

- Schneider Electric

- Siemens Energy

- Sungrow Power Supply

- Toshiba Energy Systems & Solutions

- Wartsila (formerly Wärtsilä)

{kind=link}