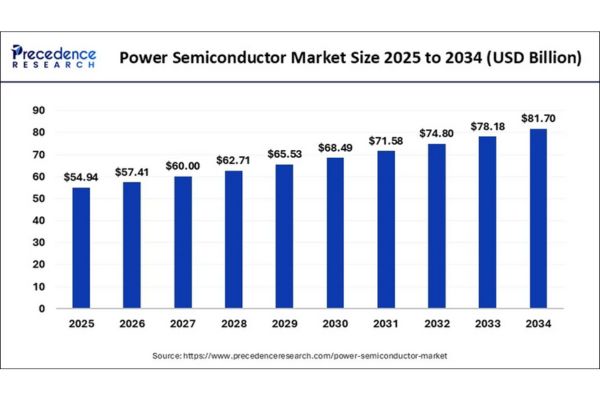

According to Precedence Research, the global power semiconductor market is set to leap from USD 52.57 billion in 2024 to nearly USD 81.70 billion by 2034, charting a strong CAGR of 4.50%.

Asia Pacific maintains its dominance, energized by government investments and tech advancements across key regional economies like China, Japan, and South Korea.

Power Semiconductor Market Key Insights

- The market was valued at USD 52.57 billion in 2024 and is expected to reach USD 81.70 billion by 2034, growing at a CAGR of 4.50%.

- Asia Pacific held the largest market share in 2024 and will likely maintain leadership, thanks to robust government support and a thriving electronics sector.

- North America is forecast as the fastest-growing region, propelled by aerospace, defense developments, and strong EV manufacturing.

- The power integrated circuits (PIC) segment led the market in 2024, while discrete components and silicon carbide materials are poised for rapid growth.

- Top companies actively driving the landscape include Toshiba Corporation, Fuji Electric, Mitsubishi Electric, Murata, Texas Instruments, and Alpha & Omega Semiconductor.

Power Semiconductor Market Revenue Outlook

| Year | Market Value (USD Billion) |

| 2024 | 52.57 |

| 2025 | 54.94 |

| 2034 | 81.70 |

Asia Pacific regional value:

- 2024: USD 21.55 billion

- 2034: USD 33.58 billion

How Is AI Accelerating the Power Semiconductor Market?

Artificial intelligence is fundamentally transforming the role of power semiconductors across major industries. AI algorithms are optimizing the design, testing, and fabrication processes, reducing errors and production costs. Machine learning-driven automation in smart factories ensures predictive maintenance, real-time quality assurance, and energy-efficient manufacturing.

Furthermore, AI-fueled demand is boosting the uptake of advanced power semiconductors in edge computing, smart consumer electronics, electric vehicles, and IoT-enabled industrial systems. This wave of innovation is tightening collaborations between chipmakers and AI innovators, propelling market growth in both high-performance and energy-economical segments.

What Is Driving Market Growth?

The relentless expansion of the home appliance and electronics sector, particularly in Asia Pacific, is a primary driver for the power semiconductor market. The region’s booming robotics industry, supported by government investments such as Japan’s US$ 13 billion push into local semiconductor manufacturing has compounded demand for advanced power management and automation technologies.

Additionally, increasing automotive electrification, alongside industrial automation upgrades, are keeping demand high for reliable, high-efficiency power semiconductors.

What New Opportunities and Trends Are Emerging?

How are Schottky barrier diodes reshaping future applications?

Schottky barrier diodes are emerging as vital components for next-gen solar cells, power transistors, and energy conversion systems. Their growing use in high-frequency, low-loss applications is creating significant opportunities for manufacturers who can innovate in this segment.

Which industry segments are outpacing the rest?

PICs (power integrated circuits) dominate due to high reliability and energy efficiency, but discrete power semiconductors are forecast to grow fastest especially in military, automotive, and industrial automation contexts. Silicon carbide materials are also seeing surging adoption in EV and renewable energy sectors because of their superior thermal and electrical properties.

What are companies doing to capture new value?

Top players are launching next-generation products, expanding partnerships, and innovating with materials like silicon carbide and gallium nitride. Leading companies Toshiba, Fuji Electric, Mitsubishi Electric, Murata, Texas Instruments, Alpha & Omega Semiconductor are increasing R&D spend and forming alliances to stay ahead of the curve.

Regional Analysis

Asia Pacific holding the biggest market share in 2024, continues to lead, benefiting from booming electronics demand, robotics adoption, and major government initiatives across Japan, China, South Korea, and India. Local champions like Toshiba and Mitsubishi are at the forefront, pushing out premium, high-efficiency chips.

North America is expected to outpace others in growth, fueled by strong demand in aerospace, defense, and the ongoing transition to electric vehicles. EV manufacturers such as Tesla, Rivian, and GM, alongside semiconductor leaders like Texas Instruments and Alpha & Omega, are driving innovation and supply chain resilience.

Segment Analysis

By Component

Power Integrated Circuits (PICs): These are semiconductor devices that combine multiple power electronic components such as transistors, diodes, and drivers into a single chip package. PICs are widely used for their compact size, energy efficiency, and reliability in power management applications. They dominate the segment due to the integration capability that allows manufacturers to save space and reduce costs in electronics like smartphones, computers, and consumer appliances.

Discrete: Discrete power semiconductors are single-function components such as diodes, thyristors, and power transistors (like MOSFETs and IGBTs). These are key in applications requiring robust, high-power performance and flexible system designs, including industrial automation, electric vehicles, and energy infrastructure. Their usage is rising rapidly in automotive and military segments due to their high switching speed and voltage-handling abilities.

By Material

Silicon/Germanium: Silicon is the traditional and still-dominant material for most power semiconductor devices, valued for its mature manufacturing technology, cost-effectiveness, and widespread compatibility. Germanium is sometimes alloyed with silicon, enhancing certain electrical properties. These materials are especially prominent in low- to mid-power applications across consumer electronics and standard industrial devices.

Gallium Nitride (GaN): Gallium Nitride is an advanced compound semiconductor material that enables devices with high breakdown voltage, low resistance, and ultra-high-speed switching. GaN power devices are quickly gaining adoption in telecom, fast-charging adapters, and radio frequency applications, where their efficiency and compactness deliver significant system-level benefits.

By End-User Industry

Automotive: The automotive sector, particularly electric and hybrid vehicles, is experiencing the fastest market growth for power semiconductors. These components are essential in advanced driver-assistance systems (ADAS), on-board chargers, electric powertrains, infotainment, lighting, and battery management. The surge in EV production and government regulations supporting clean mobility are key growth drivers in this segment.

Consumer Electronics: This industry maintains the largest market share, propelled by continuous advancements and demand for smartphones, tablets, wearables, smart household devices, and infotainment products. Power semiconductors are critical for battery management, power conversion, and voltage regulation in all these devices, ensuring efficiency, safety, and compactness.

Power Semiconductor Market Companies

- Infineon Technologies AG

- Texas Instruments Inc.

- United Silicon Carbide Inc.

- ON Semiconductor Corporation

- Renesas Electronic Corporation

- Broadcom Inc.

- ST Microelectronics NV

- NXP Semiconductor Inc.

- Toshiba Corporation

- Fuji Electric Co. Ltd

- Semikron International

- Hitachi America, Ltd.

- Wolfspeed Inc

- ROHM Co Ltd

- Vishay Intertechnology Inc.

- Nexperia BV

- Mitsubishi Electric Corporation

- Alpha & Omega Semiconductor

- Magnachip Semiconductor Corp

- Maxpower Semiconductor

- Power Semiconductors, Inc

- Microchip Technology Inc

- Littlefuse Inc.

What Challenges and Cost Pressures Do Players Face?

Despite robust demand, the market grapples with escalating raw material prices and technical complexities such as cycling resistance and decreased thermodynamic performance in harsh environments. Cost-sensitive customers, alongside increasingly sophisticated technical requirements, are pressuring firms to innovate while containing expenses.

Infineon – Case Study

Offering

Automotive-grade HybridPACK™ Drive G2 power modules (SiC + Si options) and EiceDRIVER™ isolated gate-driver ICs optimized for SiC traction inverters; first customer products built on Infineon’s 200 mm SiC wafer technology.

Project summary & timeline

- Design-win: Infineon secured a design-win to supply SiC and silicon HybridPACK™ Drive G2 modules for Rivian’s R2 traction-inverter platform, with series deliveries targeted from 2026.

- Manufacturing milestone: Advanced its 200-mm SiC roadmap and delivered the first customer products built on 200-mm SiC wafers in Q1 2025 from its Villach facility.

- Supporting products: Released new EiceDRIVER™ isolated gate drivers in 2025 to match SiC switching requirements and simplify OEM integration.

Implementation steps

- Qualified HybridPACK™ Drive G2 modules for automotive traction use against OEM and AEC-Q standards.

- Brought 200-mm SiC wafer processing online to improve cost structure and throughput.

- Introduced matching gate-driver family and reference designs to shorten customer qualification cycles.

- Coordinated pilot, PPAP, and SOP milestones with Rivian to align series-production timing.

Technical & commercial benefits

- System-level: SiC modules enabled higher efficiency, higher switching frequency, and improved inverter power density compared to traditional IGBTs.

- OEM integration: Pre-qualified modules and drivers reduced engineering time, allowing Rivian to accelerate product launch.

- Economics: 200-mm SiC wafers improved unit economics compared with smaller wafers, lowering cost per device.

Protectional / resilience measures

- Vertical investments in 200-mm SiC wafer production and in-house module assembly reduced external supply risks.

- Automotive-grade qualification provided reliability assurance to OEMs.

Outcome / market impact

- The Rivian R2 design-win positioned Infineon to capture multi-year traction module volumes starting 2026.

- Helped shift SiC adoption from premium EVs toward mainstream models by improving availability and reducing cost trajectory.

Financial after implementation

- The program created new revenue visibility through confirmed design-wins and secured mid-term growth via large EV supply contracts.

- Infineon’s SiC roadmap and HybridPACK product ramp became a key growth driver in its 2025 power-semiconductor business, strengthening its competitive position in automotive markets.

Key risks & lessons

- Risk: Delays in wafer yield improvements or module assembly could affect customer program timelines.

- Lesson: Early scaling of wafer and module capacity, combined with turnkey solutions (modules + gate drivers), is essential to secure OEM confidence and long-term contracts.

Source: https://www.precedenceresearch.com/power-semiconductor-market

{kind=link}