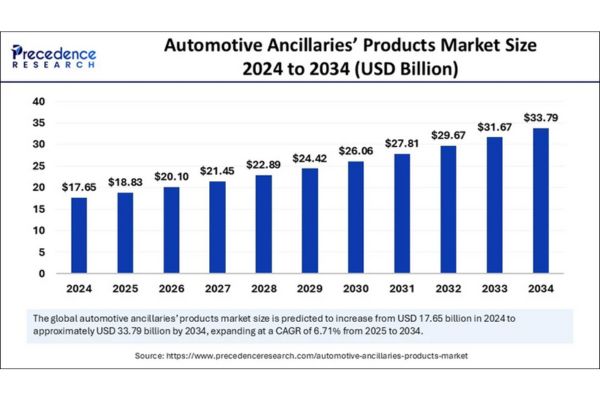

According to Precedence Research, the global automotive ancillaries’ products market is projected to grow from $18.83 billion in 2025 to an impressive $33.79 billion by 2034, expanding at a CAGR of 6.71% over this period.

This growth is fueled by rapid advancements in automotive technologies, an increasing appetite for vehicle personalization, and surging demand for electric vehicle components. As consumers and manufacturers alike push for safer, smarter, and more efficient vehicles, the ancillary products space finds itself at the forefront of innovation.

What Fuels Automotive Ancillaries’ Market Expansion?

Growth in the automotive ancillaries’ products market stems primarily from advancements in safety and performance technologies, rising consumer spending on aftermarket and OEM parts, and the accelerating shift toward electric and connected vehicles. Emerging economies, especially in Asia Pacific, continue to dominate production and consumption, while North America surges ahead as the region with the fastest growth rate.

Quick Insights: Automotive Ancillaries’ Products Market Snapshot

- The market is forecast to reach $33.79 billion by 2034.

- In 2025, market size is anticipated at $18.83 billion.

- Asia Pacific claimed top regional status with $6.88 billion in 2024, projected to double by 2034.

- North America is expected to see the fastest growth rate, driven by high vehicle ownership and EV adoption.

- Engine transmission and suspension components contribute the largest share, while electrical parts are set for rapid gains.

- Passenger vehicles lead overall demand, with commercial vehicles gaining ground due to e-commerce-driven logistics.

- The aftermarket distribution channel commands the largest share thanks to aging fleets and DIY maintenance trends.

How Is AI Transforming Automotive Ancillaries?

The infusion of Artificial Intelligence (AI) into the automotive ancillaries’ market has revolutionized design, production, and supply chain operations. Manufacturers leverage AI analysis to optimize component designs, resulting in exact, high-performing parts tested virtually before ever reaching the assembly line. AI’s predictive capabilities streamline production schedules and cost management, while its insights enable dynamic, responsive inventory control in aftermarket part supply chains.

AI also plays a vital role in enabling advanced driver-assistance systems (ADAS) and developing autonomous vehicle technologies, raising the bar for both safety and performance. As automakers and suppliers integrate AI deeper into their processes, operational productivity and innovation accelerate—giving rise to smarter components that meet the evolving demands of connected and electrified vehicles.

What Are the Key Growth Factors?

- Rising demand for personalized, safer, and high-performance vehicles.

- Continuous expansion of vehicle fleets, especially in Asia Pacific and North America.

- Shift toward sustainable mobility and green vehicle solutions.

- Aftermarket growth driven by DIY trends and widespread e-commerce reach.

- Expansion of electric vehicles requiring advanced electrical and digital ancillaries.

Which Trends and Opportunities Stand Out in This Dynamic Market?

Is Vehicle Personalization the Next Big Opportunity?

Absolutely. Customization is now a defining trend as drivers seek performance enhancement and aesthetic upgrades. From custom paint jobs to advanced suspension systems and infotainment installations, the aftermarket is booming. Specialized online platforms now make it easier than ever for consumers to access a wide array of parts, fueling further market expansion.

How Are Electric Vehicles Changing the Ancillary Market Landscape?

Electric vehicles (EVs) generate unprecedented demand for high-quality batteries, charging infrastructure, and digital components. Government incentives, especially in China and Europe, have accelerated EV adoption, making green mobility and related ancillaries hotbeds for innovation.

What’s Driving Demand for Sustainable Mobility?

Global trends toward reducing carbon emissions are propelling consumers toward EVs, with renewable energy integration and eco-friendly transport systems rising in popularity. Advanced charging systems, longer ranges, and falling vehicle costs continue to support market growth.

Regional & Segment Analysis: Who’s Fueling Growth?

Regional Leaders

Asia Pacific: Asia Pacific holds the largest market share, with its size at $6.88 billion in 2024 and projected to reach $13.35 billion by 2034 (CAGR 6.85%). This dominance stems from established automotive manufacturing hubs like China, Japan, and South Korea. China is at the forefront due to its vast vehicle production capacity, robust domestic demand, and aggressive government backing for electric vehicle (EV) adoption.

Policies supportive of green technologies have made China a global leader in EV supply chains. Technological advancements and scaling production across the region further boost the market.

North America: North America is poised for the fastest growth in the sector during the forecast period. This acceleration is driven by:

- High rates of vehicle ownership, especially in the U.S., one of the world’s largest automotive markets.

- Ongoing demand for vehicle maintenance, repair, and replacement parts due to the region’s large vehicle fleet.

- Surging adoption of EVs, with manufacturers focusing on technologies like autonomous driving, advanced connectivity, and in-vehicle infotainment systems.

Europe: Europe maintains steady growth, anchored by a strong automotive production sector and significant investments in research and development. The region features a prominent base of automotive producers, notably in Germany, France, and the UK. Strict government emissions rules and emphasis on eco-friendly transportation continue to drive demand for advanced automotive ancillaries.

Sustainability and innovation are key themes as the market adapts to evolving EU regulations and consumer preferences.

Segment Growth Highlights

By Component:

- Engine, Transmission, and Suspension Parts: These are the enduring mainstays of the market, accounting for the largest revenue share in 2024 and expected to remain dominant through 2034. The demand is propelled by the need for improved vehicle performance, engine protection, and compliance with stricter safety standards. Innovation in high-performance and fuel-efficient engines further elevates the need for advanced components.

- Electrical Parts: This segment is on a strong upward trajectory due to the accelerating expansion of EV manufacturers and the deeper integration of electronic systems in internal combustion engine vehicles. Key products include batteries, electric motors, and charging infrastructure. Investments in connected vehicle technologies (infotainment, ADAS) are also boosting demand for advanced electrical ancillaries that enhance safety, functionality, and performance.

By Application:

- Passenger Vehicles: The segment led the market in 2024—fueled by rising consumer preference for private transportation and increased disposable incomes. The trend is reinforced by the introduction of new models with upgraded safety, comfort, infotainment, and fuel efficiency features.

- Commercial Vehicles: Expected to see significant growth, this segment’s expansion is tied to the surge in global logistics and e-commerce. With higher demand for reliable delivery vehicles and trucks, manufacturers prioritize robust, high-performance ancillary products capable of enduring heavy-duty requirements.

By Distribution Channel:

- Aftermarket: Held the largest share in 2024, bolstered by aging vehicle fleets and growing consumer interest in DIY maintenance. The proliferation of e-commerce platforms further democratizes access to aftermarket parts. Connected and electric vehicle technologies are transforming the aftermarket, driving innovation in replacement parts and diagnostic solutions.

- OEM (Original Equipment Manufacturer): Forecasted for strong future growth as automakers demand parts that meet rigorous performance, quality, and safety standards. Partnerships and contractual agreements between ancillaries manufacturers and global vehicle manufacturers sustain demand in this segment.

Spotlight on Industry Breakthroughs & Leading Companies

Recent breakthroughs include next-gen suspension systems, smart sensors compatible with EVs, and advanced charging solutions. Top companies driving innovation and market growth (as listed in Precedence Research reports) include:

- Bosch

- Denso

- Magna International

- Continental

- ZF Friedrichshafen

- Aisin Seiki

- Valeo

- Aptiv

What Are the Main Challenges and Cost Pressures?

- Fluctuating Raw Material Prices: Steel, aluminum, and rubber volatility disrupts budgeting and production stability.

- Production Cost Control: Rapid innovation demands and uncertain market trends challenge manufacturers to keep costs in line without sacrificing quality.

- Sustainability Requirements: Regulatory and consumer pressure to deliver green components add complexity and expense to R&D and supply management.

Automotive Ancillaries in Action: A Case Study

In China, the integration of advanced ADAS and electrification across mainstream and high-end vehicle models shows the power of ancillaries to elevate safety and performance. Leading auto giants have slashed road accidents and boosted EV penetration rates by deploying AI-driven sensors and robust digital component platforms underscoring the vital role ancillaries play in next-generation mobility.

{kind=link}