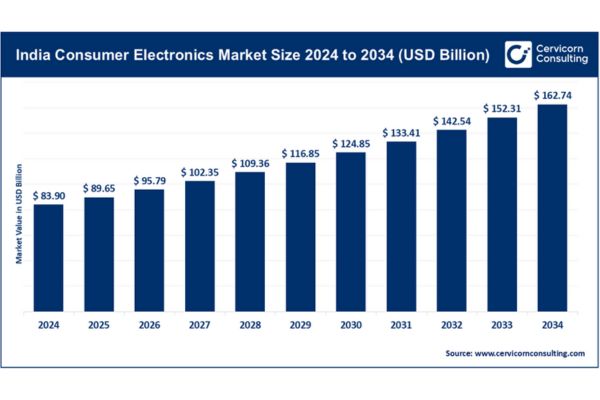

The India consumer electronics market was valued at USD 83.90 billion in 2024 and is projected to reach approximately USD 162.74 billion by 2034, expanding at a CAGR of 6.85% during 2025–2034. India is emerging as one of the fastest-growing consumer electronics markets globally, driven by rising disposable incomes, rapid urbanization, and increasing internet penetration. With a population of over 1.4 billion—of which nearly 65% falls within the working-age group—the demand for smartphones, laptops, and household appliances continues to surge.

Internet adoption, which has already crossed 850 million users, is being further accelerated by the rollout of 5G, fostering the use of smart and connected devices. Government initiatives such as “Digital India” and “Make in India” are boosting local manufacturing, reducing reliance on imports, and enhancing product accessibility for the expanding middle class. Additionally, rising awareness and preference for eco-friendly devices are contributing to market growth. The strong expansion of e-commerce has also played a vital role, offering consumers greater convenience and making India one of the fastest-growing markets worldwide.

The Indian consumer electronics sector encompasses smartphones, televisions, audio systems, wearables, and a wide range of household appliances, which significantly broadens its scope. The same underlying factors—urbanization, income growth, and digital adoption—that fueled its rise continue to create ample opportunities, underscoring the market’s long-term potential.

What are the trends of India consumer electronics market?

1. Rapid Smartphone Penetration & 5G Adoption

- Smartphones continue to lead the market, with 5G-enabled devices driving upgrades.

- Affordable data plans and increased digital consumption (social media, streaming, fintech) are boosting volumes.

- Brands are focusing on budget and mid-range devices to capture tier-2, tier-3, and rural demand.

2. E-commerce & Omnichannel Growth

- Online marketplaces (Amazon, Flipkart, Tata Cliq) are recording double-digit growth due to convenience, offers, and EMI options.

- Hybrid models like “click-and-collect” and brand-exclusive online stores are gaining traction.

- Offline retail remains strong in metros, but digital-first strategies are reshaping buying behavior.

3. Smart & Connected Devices Ecosystem

- Surge in adoption of smart TVs, wearables, and IoT-enabled appliances.

- Growing preference for integrated ecosystems (smartphones + wearables + home devices).

- Voice assistants and AI-enabled products are becoming mainstream in households.

4. Government Initiatives Boosting Local Manufacturing

- Make in India and Digital India initiatives are encouraging local production of smartphones, appliances, and components.

- Reduced dependence on imports is improving product availability and affordability.

- Production-linked incentive (PLI) schemes are drawing global manufacturers to set up in India.

5. Rural & Semi-Urban Expansion

- Rural consumption is picking up with electrification, internet penetration, and mobile connectivity.

- Affordable financing options (EMIs, digital wallets, UPI) are unlocking demand in semi-urban and rural areas.

- Brands are expanding distribution networks beyond metros to capture untapped markets.

6. Sustainability & Eco-Friendly Products

- Growing demand for energy-efficient appliances (e.g., inverter ACs, smart refrigerators).

- Eco-conscious consumers are opting for products with lower energy consumption and recyclable materials.

- Brands are marketing green electronics to appeal to the environmentally aware middle class.

7. Premiumization & Lifestyle-Oriented Demand

- Rising disposable incomes are boosting sales of premium smartphones, high-end TVs, and advanced appliances.

- Wearables and audio devices are increasingly purchased as lifestyle and fashion accessories.

- Health-focused gadgets (fitness bands, smartwatches, air purifiers) are gaining popularity.

8. Influence of E-commerce Festivals & Discounts

- Annual sales events like Flipkart’s Big Billion Days and Amazon’s Great Indian Festival drive massive spikes in electronics sales.

- Seasonal promotions and cashback offers significantly influence consumer buying patterns.

India Consumer Electronics Market – Segmental Analysis

Product Type Analysis

Smartphones: Smartphones dominate the market, accounting for nearly 40% of total share. Growth is fueled by widespread adoption of 4G and 5G networks, affordable data packages, and rising demand for multifunctional devices. Leading brands such as Samsung, Xiaomi, and Vivo collectively sell over 200 million units annually, expanding their presence across urban and semi-urban regions.

Televisions: Smart televisions hold the second-largest market share, contributing around 20%. Rising demand for home entertainment, coupled with increased streaming subscriptions, has accelerated adoption. Sales in metro cities alone have grown by over 15% annually, highlighting the shift toward connected entertainment solutions.

Wearables: Wearables—including smartwatches and fitness bands—have gained strong traction, particularly among health-conscious consumers. Integration with smartphones and IoT devices has fueled steady growth, with the segment expanding by approximately 18% in the past three years.

Home Appliances: Refrigerators, air conditioners, and washing machines collectively account for about 25% of the market. An additional 15% share is held by personal care electronics and audio devices, both witnessing steady growth due to rising disposable incomes and lifestyle-driven spending.

Distribution Channel Analysis

Offline Retail: Traditional retail, comprising specialist electronics stores, hypermarkets, and multi-brand outlets, continues to lead with nearly 55% market share. Brands such as Croma, Reliance Digital, and Vijay Sales dominate tier-1 and metropolitan cities, where consumers still value hands-on experience and immediate product availability. However, growth in this channel has moderated to around 8% annually, as online competition intensifies.

E-commerce Platforms: Online marketplaces—including Amazon, Flipkart, and Tata Cliq—represent the fastest-growing channel, capturing around 35% of the market and posting a CAGR of 20–22% over the last three years. Growth is largely driven by convenience, competitive pricing, and digital payment adoption, with significant penetration in tier-2 and tier-3 cities.

Direct Sales: Direct-to-consumer sales account for roughly 10% of the market. Brands like Apple and Samsung leverage this model to strengthen brand loyalty, offer exclusive products, and deliver premium post-sale support. Hybrid models—such as click-and-collect—are also gaining traction as consumers increasingly value flexibility.

End-User Analysis

Urban Consumers: Urban buyers contribute nearly 60% of transactions, supported by higher disposable incomes, digital-savvy lifestyles, and strong demand for premium and mid-range products. Annual smartphone purchases in urban areas already surpass 100 million units, further accelerated by e-commerce and organized retail growth.

Tier-1/2/3 Cities: Semi-urban consumers account for about 25% of market share, driven by demand for budget smartphones, LED TVs, and home appliances. Expanding internet access, digital wallets, and EMI-based financing options have boosted affordability, resulting in sales growth of 12–15% annually in these regions.

Rural Consumers: Rural areas currently represent 15% of the market but hold immense growth potential. Government-led digitalization programs, rural electrification, and improved mobile connectivity are driving adoption of budget smartphones and basic appliances. However, challenges such as limited retail access, low brand awareness, and price sensitivity remain. To address this, brands like Xiaomi, Samsung, and LG are expanding distribution networks, blending offline and online channels to penetrate deeper into rural markets.

{kind=link}