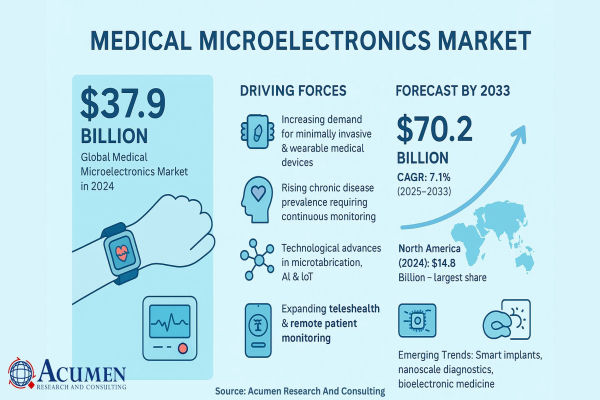

The Medical Microelectronics Market—driven by miniaturized implants, diagnostic wearables, and remote monitoring devices—is growing rapidly. According to Acumen Research & Consulting, this sector is poised to expand from USD 37.9 billion in 2024 to USD 70.2 billion by 2033, with a solid 7.1% CAGR over 2025–2033.

Market Size, Forecast & Key Insights

- Market Size (2024): USD 37.9 B

- Forecast (2033): USD 70.2 B

- Compound Annual Growth Rate (2025–2033): 7.1%

This growth trajectory reflects strong adoption of diagnostic, monitoring, and therapeutic microelectronic devices across implantable and wearable categories.

What Is Medical Microelectronics?

Medical microelectronics integrates miniature electronic systems—including sensors, ICs, MEMS, displays, and actuators—into devices for diagnostics, therapeutics, monitoring, and drug delivery. From implantable pacemakers and neurostimulators to wearable glucose monitors and lab-on-a-chip diagnostics, these technologies are redefining precision care.

Key innovations accelerating adoption include:

- Microfabrication techniques (photolithography, etching) enabling ultra-compact designs

- Smart closed-loop systems for adaptive therapy (e.g. in neuromodulation)

- Biodegradable and wireless power-enabled implants to reduce surgical burden

Medical Microelectronics Market Regional Outlook

North America: Market Leader

In 2024, North America held the largest share—approximately USD 14.8 billion, or nearly 39% of the global market. The region’s dominance stems from advanced healthcare infrastructure, high patient adoption of remote patient monitoring technology, and rapid deployment of AI-enhanced implants. Some of the prominent factors driving the growth of medical microelectronics market in this region include:

- Regulatory environment encouraging advanced devices—e.g., Medicare expansion of telehealth services through 2025

- Leading manufacturers such as Medtronic, Abbott, Boston Scientific, GE Healthcare, and Philips operating locally

- High R&D capacity and clinical adoption for AI-powered wearable and implantable microelectronic platforms

Asia-Pacific: Fastest-Growing Market

Asia-Pacific is the fastest-growing region, with a forecasted 8% CAGR, capturing over 30% of the market share in 2023. Key regional growth factors include:

- Expansion of healthcare infrastructure across China, India, and Southeast Asia

- Rising demand for chronic disease management devices—especially pacemakers, neurostimulators, and wearable monitors

- India’s microelectronics implants market projected to grow from USD 1.4 Billion in 2024 to USD 2.5 Billion by 2032 (CAGR 8.5%)

Europe: Technology + Regulation-Driven Growth

Europe accounted for roughly 22% of global revenue in 2023, and is expected to maintain steady growth, supported by strong regulatory frameworks (e.g., EU MDR, cybersecurity mandates), and robust adoption of monitoring implants and lab-on-chip diagnostics.

Highlights:

- Emphasis on data security and medical device compliance

- High penetration of AI-enabled diagnostic devices

- Advances in biomEMS and integrated diagnostics for personalized care

Latin America & Middle East & Africa: Emerging Opportunity Zones

These regions collectively represent approximately 10% of the market, characterized by:

- Moderate healthcare penetration, expanding with government reforms

- Growing adoption of portable diagnostic and monitoring devices

- Early interest in implantable microelectronics, and increasing engagement in emerging technologies for remote care delivery

Applications & Segment Dynamics

- Implantable Devices: Pacemakers, neurostimulators, cochlear implants dominate the implantable microelectronics segment—accounting for ~60% of the total revenue in 2023.

- Non-Implantable/Wearables: Accelerating at ~9% CAGR, driven by demand for real-time monitoring devices like glucose meters, wearable ECG patches, and pulse oximeters.

- Applications: Diagnostic and therapeutic applications account for nearly 70% of usage, with research and biotech uses expanding at ~10% annual growth.

Key Trends & Innovation Trajectory

The Medical Microelectronics Market is being fundamentally reshaped by converging breakthrough technologies—creating smarter, safer, and more autonomous patient care systems. Emerging trends in device miniaturization, connectivity, AI integration, wireless energy, and regulatory evolution are leading the innovation trajectory. Below is an enhanced and detailed analysis of these key trends:

1. AI & Smart Microelectronics: Toward Adaptive, Closed‑Loop Systems

Artificial intelligence and machine learning are deeply influencing implantable and wearable device functionality. AI-driven sensors and algorithms enable real-time diagnostic feedback, predictive analytics, and therapy adjustments embedded directly into the device. For instance, AI-enhanced neurostimulators can detect symptom states and automatically modulate stimulation parameters accordingly—ushering in closed-loop medical systems that adapt to individual patient physiology. In parallel, the FDA’s Digital Health Center of Excellence has authorized hundreds of AI/ML-enabled devices since 2020, and issued draft guidance in 2025, signaling regulatory commitment to advancing smart medical electronics.

2. Ultra‑Miniaturization & Bio-MEMS Integration

Ongoing progress in microfabrication (e.g. MEMS, micro-etching, Bio-MEMS) allows devices to shrink dramatically while enhancing functionality. Microneedle arrays, flexible implantables, and surgical micro-tools integrate sensors for temperature, pressure, and chemical detection. These devices enable minimally invasive surgical approaches, deployable diagnostic patches, and embedded drug-delivery systems—often with improved biocompatibility and reduced scarring.

3. Wireless Power Transfer & Energy Harvesting Solutions

Wire-free operation is revolutionizing implant lifecycle and patient convenience. Techniques such as inductive coupling and ultrasonically powered communication are powering deep implants—eliminating battery replacement surgeries. Hybrid wireless schemes provide both power and bi-directional data flow, optimizing safety and implant longevity. Research continues to refine energy harvesting from motion, heat, and even blood flow.

4. Body Area Networks & Bio‑Converged Connectivity

Implants and wearables are increasingly interconnected via Body Area Networks (BAN/WBAN), enabling real-time data aggregation and transmission to clinicians or AI-driven monitoring platforms. These networks integrate wireless protocols like Bluetooth, Wi‑Fi, and ultra-low-power radio, forming a secure medical IoT ecosystem. BANs allow remote monitoring and swift intervention—central to remote healthcare and value-based care models.

5. Biodegradable & Temporary Electronics

Disposable and bioresorbable electronics—designed to function and dissolve post-therapy—are emerging as critical innovations. Such devices eliminate the need for surgical removal and have applications in short-term diagnostic monitoring or temporary localized therapy. This trend is beneficial for controlled drug release systems, wound monitoring implants, and temporary neuromodulation tools.

6. Expansion into Brain–Computer Interfaces (BCIs) & Neural Implants

Advanced neural implants and intelligent interfaces are transitioning from concept to reality with embedded signal processing modules and adaptive stimulation capabilities for movement recovery, psychiatric therapies, and communication in paralyzed patients. Trailblazing research in Europe and North America highlights potential markets worth hundreds of billions of dollars, necessitating secure microelectronics for sensor arrays, signal amplification, and wireless control—alongside ethical frameworks ensuring neural data privacy.

7. Integration of Telehealth, IoMT & Remote Monitoring

Microelectronic implants and wearables are central to telemedicine and remote chronic disease management. Patients using implantable cardiac monitors, glucose sensors, or wearables can transmit data continuously for clinician review. Regulatory adoption and remote care reimbursement policies are fast-tracking these devices into mainstream care, emphasizing preventive health and proactive therapy adjustments.

8. Cybersecurity & Regulatory Maturation

With connected medical devices comes increased cybersecurity and data privacy risk. Regulators in North America and Europe have updated device classifications and guidance—mandating encryption, authentication protocols, and lifecycle vulnerability management. Manufacturers must align microelectronics design with new MDR and AI/ML medical device frameworks, while regulatory science tools and advisory programs (e.g. FDA’s TAP) support accelerated innovation.

9. Bioconvergence: Bridging Biology, Engineering & Data Science

Medical microelectronics increasingly intersect with biotechnology, nanoscience, robotics, and AI—a paradigm referred to as bioconvergence. This multidisciplinary synthesis supports next-generation implantable sensors, synthetic biological interfaces, and cloud-connected analytics solutions—transforming medical microelectronics into intelligent diagnostic and therapeutic platforms in both surgical and chronic settings

Strategic Recommendations

For Device Manufacturers:

- Accelerate integration of wireless power, biodegradable materials, and micro-sensors

- Prioritize regulatory readiness for upcoming cybersecurity requirements and device classification pathways

- Consider geographic strategy: prioritize implantable device rollouts in North America; focus on wearables and emerging markets in Asia-Pacific

For Healthcare Providers & Researchers:

- Deploy miniaturized diagnostic tools to enable remote monitoring and telehealth service delivery

- Collaborate with AI and microelectronics innovators to pilot adaptive therapy systems

For Investors & Policymakers:

- North America offers mature market access with regulatory transparency and high ROI in complex implants

- Asia-Pacific presents attractive growth in mid-tech segments (e.g. wearables, diagnostics) with rapidly improving infrastructure and healthcare funding

Market Snapshot & Takeaways

- Size (2024): USD 37.9 B → Forecast (2033): USD 70.2 B (7.1% CAGR)

- Regional Leaders: North America (~39% share), Asia-Pacific (~30%), Europe (~22%)

- Fastest Growth: Asia-Pacific (~8% CAGR), followed by Europe and modest Latin America expansion

- Applications: Implantables dominate; wearables rise rapidly in non-implantable segments

{kind=link}