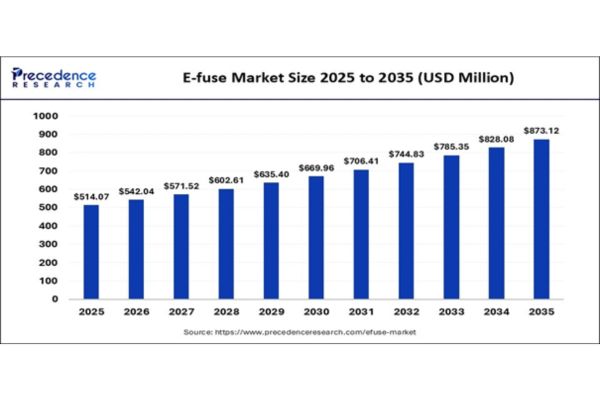

The global e-fuse market size accounted for USD 514.07 million in 2025 and is predicted to increase from USD 542.04 million in 2026 to approximately USD 873.12 million by 2035, expanding at a CAGR of 5.44% from 2026 to 2035.

AI E-fuse Market Key Insights

- The Asia Pacific accounted for the largest market share of 40.4% in 2025 and is set to grow at the fastest CAGR of 6.5% from 2026 to 2035.

- North America is expected to rise at a notable CAGR between 2026 and 2035.

- By type, the programmable e-fuse segment has contributed the largest market share of 72.5% in 2025.

- By type, the non-programmable e-fuse segment is growing at a CAGR of 5.8% between 2026 and 2035.

- By voltage rating, the 5V-20V segment held the largest market share of 43.5% in 2025.

- By voltage rating, the above 40V segment is poised to grow at a CAGR of 5.7% between 2026 and 2035.

- By application, the consumer electronics segment captured the highest market share of 32.5% in 2025.

- By application, the automotive electronics segment is growing at a CAGR of 5.5% between 2026 and 2035.

- By distribution channel, the direct sales segment accounted for the biggest market share of 56.8% in 2025.

- By distribution channel, the online sales segment is expanding at a strong CAGR of 5.6% between 2026 and 2035.

Market Overview of E-fuse Market

The e-fuse market is growing rapidly as manufacturers increasingly shift toward intelligent, secure, and dependable electronic protection technologies. Electronically controlled fuses are becoming essential as compact, high-density electronics are deployed across consumer devices, automotive electronics, and industrial control systems. Traditional mechanical fuses are limited in response speed and diagnostics, while e-fuses enable programmable current limiting, fault detection, and real-time monitoring.

Growing investments in advanced power management integrated circuits and the industry-wide push toward smaller, more efficient circuit designs further support market expansion. These trends are particularly visible in applications where board space is limited, and protection accuracy directly affects system reliability.

Regional Outlook for E-fuse Market

North America is growing rapidly, with notable market share, backed by widespread use of high-reliability circuit protection across industries such as digital devices, data infrastructure, and next-generation mobility. The demand for programmable e-fuses is increased by the region’s high safety standards, quick technological advancements, and rising investment in sophisticated power systems. It’s a quick technological advancement and a rising investment in sophisticated power systems. Its quick expansion is fueled by ongoing modernization in energy and industrial applications.

Asia Pacific dominates the e-fuse market due to its extensive electronics manufacturing ecosystem and sustained demand for advanced circuit protection technologies. The region hosts large-scale production of smartphones, consumer appliances, automotive electronics, and industrial automation equipment, all of which require compact and reliable protection components.

Rapid technological advancement, expanding semiconductor fabrication capacity, and continuous miniaturization of electronic products are driving strong adoption of programmable e-fuses. Increasing investment in power management components and local semiconductor supply chains further reinforces the region’s leading position.

Europe shows steady growth driven by increasing modernization across key electronic applications and a strong emphasis on dependable, energy-efficient power systems. Regulatory focus on safety compliance and product reliability encourages manufacturers to adopt advanced protection technologies that offer diagnostics and controlled fault response. The integration of smart e-fuse solutions is supported by the region’s adoption of next-generation device architectures in automotive electronics, industrial automation, and renewable energy systems. Growing investment in digital infrastructure and electrified transport continues to support market expansion.

Market Scope

| Report Coverage | Details |

| Market Size in 2025 | USD 514.07 Million |

| Market Size in 2026 | USD 542.04 Million |

| Market Size by 2035 | USD 873.12 Million |

| Market Growth Rate from 2026 to 2035 | CAGR of 5.44% |

| Dominating Region | North America |

| Fastest Growing Region | Asia Pacific |

| Base Year | 2025 |

| Forecast Period | 2026 to 2035 |

| Segments Covered | Type, Voltage Rating, Application, Distribution Channel, and Region |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Segmental Insights of E-fuse Market

By Type Insights

Why Did the Programmable E-fuse Segment Dominate the Market?

Programmable E-fuse: This segment dominates the market with a 72.5% share because of its versatility, cutting-edge security features, and extensive use in contemporary small electronics. They are crucial for next-generation devices because they provide real-time monitoring, automatic reset, and adjustable current limits. Programmable variations are becoming more popular in industries such as consumer electronics, telecom, and industrial automation to improve circuit safety and reliability.

By Voltage Rating Insights

Why Did the 5V-20V Voltage Segment Dominate the E-fuse Market in 2025?

5V-20V: This category dominates with 43.5% market share, as it is compatible with the widest range of common electronic devices. This range is favored for wearables, computing peripherals, smartphones, and portable devices, all of which account for enormous global manufacturing volumes. The increasing integration of power-efficient components has further bolstered demand in this voltage.

Above 40V: The segment is growing fastest, at 5.7%, as high-voltage systems are used more frequently in sectors such as renewable energy, automotive, and industrial automation. Advanced e-fuses are essential for these applications because they provide robust protection against electrical faults and high-current spikes. The expansion of solar inverters and electric vehicles is accelerating uptake in this category.

By Application Insights

What Made the Consumer Electronics Segment Dominate the Market?

Consumer Electronics: The segment dominates the application landscape, with a 32.5% share, driven by the large scale production of smartphones, laptops, wearables, and smart home devices. These products require compact, reliable, and programmable e-fuses to support modern miniaturized circuit designs. The continuous launch of high-performance gadgets keeps this segment at the forefront of demand.

Automotive Electronics: This segment is the fastest-growing segment at 5.5% propelled by digital cockpit technologies, advanced driver assistance systems, and growing EV adoption. More sensitive high power electronic modules are used in vehicles today, necessitating accurate and quick protection. The market for automotive-grade e-fuses is growing due to the electrification trend.

By Distribution Channel Insights

Why Did the Direct Sales Segment Dominate the Market?

Direct Sales: The segment led the e-fuse market by accounting for a 56.8% market share. This dominance is driven by the technical complexity of e-fuse integration and the need for close coordination between manufacturers and end users during product selection and deployment. Large OEMs in automotive electronics, industrial automation, power management, and consumer electronics often require customized e-fuse specifications related to current thresholds, thermal limits, fault response timing, and programmability.

Recent Developments

- In December 2025, Toshiba Electronic Devices & Storage Corporation announced the launch of its new 40V TCKE 6 series eFuse ICs, designed for enhanced overcurrent and overvoltage protection in compact designs. The solution targets industrial, consumer, and battery-powered devices needing fast, precise circuit protection

- In August 2025, Alpha and Omega Semiconductor launched the AOZ17517 QI 60A eFuse, which built the high-reliability 12V power rails used in cloud servers, AI processors, and telecom systems. It offers programmable protection, faster fault isolation, and improved thermal performance.

E-fuse Market Companies

Semiconductor Components Industries, LLC is a leading supplier of intelligent power and sensing technologies for automotive, industrial, and cloud power applications. The company focuses on energy-efficient semiconductor solutions that support electric vehicles, automation, and renewable energy systems.

Texas Instruments Incorporated is a global semiconductor company known for its analog chips and embedded processors used in industrial, automotive, and consumer electronics. Its innovations support power management, signal processing, and smart electronic devices worldwide.

Alpha and Omega Semiconductor specializes in power semiconductors, including MOSFETs and power ICs for computing, consumer electronics, and industrial applications. The company is recognized for improving power efficiency and thermal performance in electronic systems.

Analog Devices, Inc. develops high-performance analog, mixed-signal, and digital signal processing technologies. Its solutions are widely used in automotive, healthcare, industrial automation, and communications industries.

Diodes Incorporated manufactures discrete, logic, analog, and mixed-signal semiconductors for automotive, industrial, and consumer electronics markets. The company is known for delivering energy-efficient and cost-effective semiconductor solutions.

Bel Fuse Inc. designs and manufactures power, protection, and connectivity products used in networking, telecommunications, and industrial sectors. The company provides reliable circuit protection and magnetic solutions for advanced electronic systems.

SCHURTER AG is a Swiss technology company specializing in electronic components such as fuses, connectors, switches, and EMC products. Its products are widely used in medical equipment, industrial automation, and energy applications.

Eaton Corporation plc provides intelligent power management solutions for electrical, aerospace, hydraulic, and vehicle industries. The company focuses on energy-efficient technologies that improve safety, reliability, and sustainability.

Siemens AG is a global leader in industrial automation, smart infrastructure, mobility, and digital transformation technologies. The company develops innovative solutions for energy management, healthcare, and manufacturing industries.

ABB Ltd specializes in electrification, robotics, automation, and motion technologies for industrial and utility sectors. The company plays a key role in advancing smart factories, renewable energy integration, and sustainable infrastructure.

{kind=link}